Yes, you can finance or lease a used car in the UAE. Here’s what you need to know:

-

Financing: Banks and platforms offer loans for used cars with interest rates between 3%–7%, or as low as 1.99% for eligible applicants. A 20% down payment is required, and loans typically cover cars up to 5–7 years old, with some banks extending this to 10 years.

-

Leasing: Leasing is ideal for short-term residents or those preferring lower monthly payments. Lease costs can be up to 40% lower than new car leases and often include maintenance, insurance, and registration. However, options for used car leases are limited.

-

Eligibility: Minimum salary requirements range from AED 3,000–AED 5,000. A credit score of 650+ improves approval chances. Documents like Emirates ID, salary certificate, and bank statements are required.

-

Challenges: Down payments, vehicle age restrictions, and valuation requirements can complicate the process. Banks only finance 80% of the car’s appraised value, and a valuation certificate (AED 300–AED 500) is needed.

Quick Tip: Platforms like YallaMotor simplify the process with online tools for comparing offers, valuation, and fast approvals.

Key Decision: Financing suits those seeking long-term ownership, while leasing is better for flexibility and lower upfront costs.

How to Buy a Car in UAE Made Easy! FULL GUIDE!

Common Problems with Financing and Leasing Used Cars in the UAE

Financing or leasing a pre-owned vehicle in the UAE can seem straightforward, but certain hurdles may complicate the process. Being aware of these challenges - like down payment requirements, vehicle age restrictions, and limited leasing options - can help you prepare better and avoid surprises.

Down Payment Requirements for Used Cars

The UAE Central Bank sets a minimum 20% down payment for all car loans, but lenders often ask for 25% to 30% when it comes to used cars. This depends on factors like the car's age, condition, and even your credit history. For buyers juggling multiple financial responsibilities, this upfront cost can be a significant strain.

Some promotions advertise "0% down payment" deals, but these are usually structured as separate personal loans to cover the deposit. While they might sound appealing, they come with higher interest rates overall. Additionally, banks will only finance 80% of the car's value as determined by their authorised valuator - not necessarily the seller's price. If the valuator appraises the car at a lower price than the asking amount, you’ll need to cover the difference out of pocket. A valuation certificate, which costs between AED 300 and AED 500, is typically required for this process. Beyond the deposit, the car’s age and condition are also critical factors in determining loan eligibility.

Age and Condition Limits on Vehicles

Most banks in the UAE only finance cars that are 5 to 7 years old, with some extending this limit to 10 years. However, the "age at completion" rule is key: the car must not exceed 10 years by the time the loan is fully repaid. For instance, if you’re eyeing an 8-year-old car, your loan term might be capped at 2 years instead of the usual 5 years.

Banks also require a valuation certificate to confirm the car’s condition, and comprehensive insurance is mandatory throughout the loan period. These restrictions apply to both loans and leases, which can narrow your options significantly.

Few Leasing Options for Pre-Owned Vehicles

Leasing a used car is far less common than leasing a new one. Older cars come with higher mechanical risks, especially in the UAE's harsh climate, where extreme heat can speed up wear and tear on tyres, batteries, and other components. This added maintenance burden makes leasing companies hesitant to offer plans for older vehicles.

Another challenge is depreciation. Since used cars have already lost much of their value, it’s harder for leasing companies to predict future worth and design competitive lease agreements. Banks and financial institutions also tend to offer better interest rates and simpler processes for new or nearly new cars.

While some agencies provide short-term leases - usually 12 to 24 months - for used cars to accommodate temporary residents, these options are rare compared to traditional bank loans or Islamic financing.

How to Finance a Used Car in the UAE

Financing a used car in the UAE is straightforward, with options available through both conventional and Shariah-compliant methods. Many major banks offer financing for pre-owned vehicles for up to 60 months, covering as much as 80% of the car's value. Here's a closer look at some of the top bank options and their terms for used car financing.

Bank Financing Plans for Used Cars

Several banks in the UAE provide attractive options for used car financing. Emirates Islamic offers Shariah-compliant auto finance starting at a 3.19% flat rate per annum. Loans can go up to AED 1,500,000, with a minimum salary requirement of AED 4,000 for salaried individuals. For self-employed applicants, the income threshold is higher at AED 20,000 per month. Additionally, they offer a 60-day grace period before the first instalment.

Emirates NBD finances vehicles up to 12 years old, with interest rates ranging from 2.99% to 4.90%, depending on the customer's profile and the plan. The minimum salary requirement is between AED 4,000 and AED 5,000. Abu Dhabi Islamic Bank (ADIB) starts its rates at 3.25% flat for salary transfer customers and finances cars as old as 2008 models, with a required minimum salary of AED 5,000. Across the board, interest rates for used car loans tend to fall between 2.5% and 4.5%.

For Islamic financing, banks use a Murabaha structure. This means the bank purchases the car and then resells it to the buyer at a declared profit margin. This setup ensures fixed instalments throughout the loan term and eliminates hidden fees.

What You Need to Qualify for Financing

To qualify for a used car loan, most banks require applicants to be aged between 21 and 65 years. However, some Islamic banks may accept applicants as young as 18. Salaried employees usually need to have at least six months of tenure with their current employer, while self-employed individuals must show two years of stable business operations. A solid credit score is also key - typically, a score of 650 or higher is necessary to secure competitive rates, and a score above 700 can greatly improve your chances of approval. Additionally, banks will assess your Debt Burden Ratio to ensure your total monthly loan payments do not exceed 50% of your income after accounting for other liabilities.

The required documents include:

-

A valid passport with residence visa

-

Emirates ID

-

UAE driving licence

-

Salary certificate (dated within 30 days)

-

Three to six months of official bank statements

For the car itself, you'll need a dealer quotation or pro-forma invoice, a valuation certificate, and the ownership title (Mulkiya). Self-employed applicants must also provide a trade licence, Memorandum of Association (MOA), and six months of business bank statements.

Processing fees are typically 1.05% of the loan amount, capped at AED 2,500 to AED 2,625. Comprehensive insurance is mandatory for the loan's duration, with the bank listed as a co-beneficiary.

How YallaMotor Helps with Financing

After meeting the eligibility criteria, YallaMotor simplifies the financing process through its digital platform, powered by FinMart. This platform allows you to compare multiple bank offers in one place, avoiding the need to visit individual banks. You can access exclusive rates and handle the entire application process online, saving both time and effort. The platform tailors its recommendations based on your salary, credit score, and the car's age and value.

YallaMotor also uses AI-powered valuation tools to help you determine a fair price for the vehicle. This ensures that the authorised valuator assesses the car at a value close to your expectations, reducing the chances of unexpected out-of-pocket expenses.

How to Lease a Used Car in the UAE

Leasing a pre-owned car in the UAE might not be as popular as financing, but it’s a practical option for those looking for lower monthly payments and an easier paperwork process. Providers in the UAE offer leasing plans designed to fit different budgets, making it a viable choice for many. Here's a closer look at some key leasing options.

Shariah-Compliant Leasing Through Murabaha

For those seeking Islamic finance-compliant options, leasing through the Murabaha model is a solid choice. In this structure, the leasing company purchases the car and sells it to you at a fixed profit margin with deferred payments. This approach ensures complete transparency - no hidden fees, and you know the total cost upfront. Unlike Ijarah (another Islamic leasing option) where the bank owns the car during the lease period, Murabaha gives you full ownership of the vehicle immediately. Monthly instalments are fixed, and some agreements even allow for early settlement.

Leasing Certified Pre-Owned Vehicles

Certified pre-owned (CPO) leasing programmes take the benefits of leasing a step further by ensuring quality and reliability. These vehicles undergo detailed multi-point inspections - often covering around 125 checks - to meet manufacturer standards for age and mileage. Many of these programmes bundle essential services like maintenance, insurance, registration, and roadside assistance into a single monthly payment, making budgeting much easier and reducing unexpected expenses.

For instance, lease-to-own programmes for used cars in Dubai start at approximately AED 5,500 per month. After a typical term of 12 to 36 months, you can take full ownership by paying a nominal fee of around AED 1,000. Companies like Takeauto boast a 98% approval rate for their lease-to-own plans, thanks to minimal documentation requirements. Over the past 2.5 years, they’ve facilitated the sale of more than 300 cars through these programmes.

YallaMotor's Leasing Solutions

YallaMotor offers a convenient way to explore leasing options alongside financing. Through their platform, powered by FinMart, you can access and compare multiple leasing and financing offers from a variety of banks and providers - all in one place. This digital solution saves time by eliminating the need to visit individual branches. Plus, the platform tailors recommendations based on your profile, helping you find competitive rates and terms that work for you.

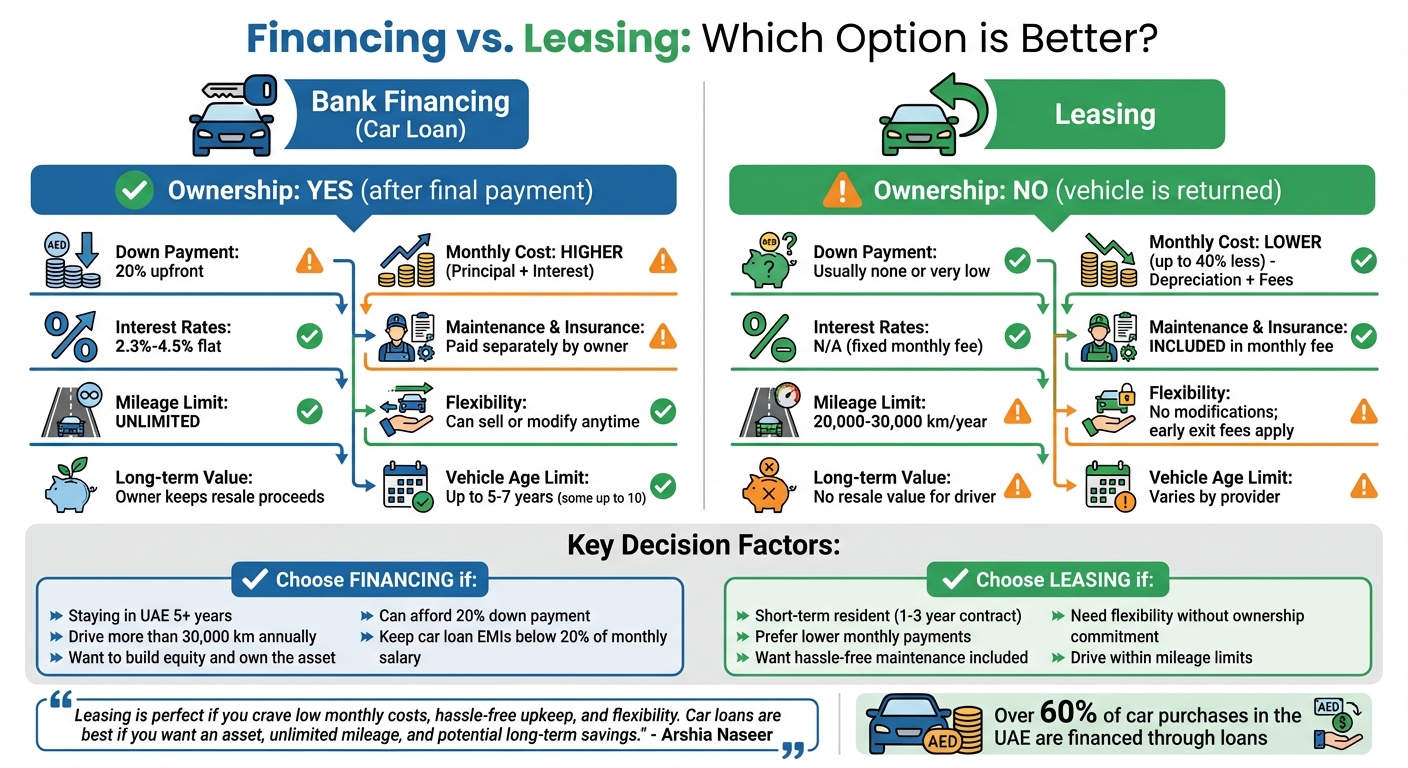

Financing vs. Leasing: Which Option is Better?

Used Car Financing vs Leasing in UAE: Complete Comparison Guide

Deciding between financing and leasing often comes down to your budget, how long you plan to stay in the UAE, and whether you prefer owning a car or not. Each option has its own set of benefits and trade-offs, especially when it comes to monthly expenses, flexibility, and long-term value.

Financing means taking out a loan, typically requiring a 20% down payment, with interest rates ranging from 2.3% to 4.5% flat per annum. Once you've paid off the loan, the car is yours. Monthly payments tend to be higher because you're covering the vehicle's full value along with interest. However, financing gives you ownership, allowing you to sell or modify the car as you wish.

Leasing, on the other hand, works like a long-term rental. At the end of the lease, you return the car unless you opt for a buyout. Monthly payments are lower - sometimes up to 40% less than financing a new car - because you're only paying for depreciation and services such as insurance, maintenance, and registration. The downside? You won’t own the car, and leases often come with mileage limits.

"Leasing is perfect if you crave low monthly costs, hassle‑free upkeep, and flexibility. Car loans are best if you want an asset, unlimited mileage, and potential long‑term savings." - Arshia Naseer

Here’s a quick comparison of the two options:

Financing vs. Leasing Comparison Table

|

Feature |

Bank Financing (Car Loan) |

Leasing |

|---|---|---|

|

Ownership |

Yes, after final payment |

No, vehicle is returned |

|

Down Payment |

20% upfront |

Usually none or very low |

|

Monthly Cost |

Higher (Principal + Interest) |

Lower (Depreciation + Fees) |

|

Maintenance & Insurance |

Paid separately by owner |

Included in monthly fee |

|

Mileage Limit |

Unlimited |

20,000–30,000 km/year |

|

Flexibility |

Can sell or modify anytime |

No modifications; early exit fees |

|

Long-term Value |

Owner keeps resale proceeds |

No resale value for driver |

|

Interest Rates |

2.3%–4.5% flat |

N/A (fixed monthly fee) |

|

Vehicle Age Limit |

Up to 5–7 years (some up to 10) |

Varies by provider |

What to Consider When Choosing

To make the right choice, think about your driving habits, financial situation, and how long you plan to keep the car.

If you're staying in the UAE for five years or more, financing could save you money in the long run. Once your loan is paid off, monthly payments stop, and you can recover some of your investment by selling the car. For expats or short-term residents on 1–3 year contracts, leasing is often a better fit. It offers lower upfront costs, includes maintenance, and avoids the commitment of ownership.

Your budget is another critical factor. Experts suggest keeping car loan EMIs below 20% of your monthly salary. If the 20% down payment for financing feels out of reach, or you prefer predictable monthly costs that cover insurance and servicing, leasing might be more practical. However, if you drive more than 30,000 km annually, financing is the better choice due to mileage restrictions on leases.

Lastly, remember that total costs go beyond monthly payments. With financing, you'll need to manage insurance, maintenance, and registration separately, which can add up. Leasing bundles these into a single payment, but you won’t build equity. Also, check your credit score - ideally 650+ - to qualify for the best financing rates.

How to Finance or Lease a Used Car with YallaMotor

YallaMotor simplifies the process of checking a car's value and securing financing or leasing options, all in one seamless platform. No more running back and forth between banks - everything you need is just a few clicks away.

Let’s break it down step by step.

Step 1: Check Your Car's Value with YallaMotor

Before diving into financing or leasing, it’s important to know the car’s market value. YallaMotor’s Car Valuation tool makes this easy. Powered by AI, the tool provides an instant estimate of the vehicle’s worth, helping you avoid overpaying and giving banks a clear idea of the financing amount they can offer.

Here’s the best part: while traditional valuation certificates from independent inspectors can cost between AED 300 and AED 500, YallaMotor’s tool gives you a quick and hassle-free estimate without extra fees. Having this information upfront not only strengthens your bargaining power with sellers but also helps you sidestep potential financing issues later.

Step 2: Find Certified Used Cars on YallaMotor

Once you’ve got the valuation sorted, head over to YallaMotor’s Certified Pre-Owned section. Here, you’ll find cars that have passed a thorough 175-point inspection. These vehicles come with added perks like a warranty and a 30-day return policy, ensuring peace of mind.

Banks and leasing companies are more likely to approve financing for these professionally vetted cars. Plus, YallaMotor takes the guesswork out of budgeting by displaying estimated monthly instalments on each listing. For example, a 2024 Toyota Corolla might show an estimated payment of AED 745 per month. Some listings even feature "Zero Down Payment" options, making it easier to secure financing without a hefty upfront cost.

Step 3: Compare Financing and Leasing Options

After selecting your car, it’s time to explore financing or leasing terms that fit your budget. YallaMotor’s platform handles the entire loan process, offering competitive rates and even Sharia-compliant Murabaha options. Interest rates typically range from 2.5% to 4.5%, with loan terms of up to 60 months.

To get started, you’ll need a few key documents: three to six months’ worth of bank statements, a salary certificate, and proof of a minimum monthly salary between AED 3,000 and AED 5,000. With everything in place, you’ll be ready to drive off in your dream car without unnecessary delays.

Conclusion: Choose the Right Option for Your Budget

When it comes to financing or leasing a used car in the UAE, both options have their merits. If you're looking for long-term ownership and the potential to build equity, financing might be the better fit. On the other hand, leasing is ideal if you prefer lower monthly payments and more flexibility. The choice ultimately depends on how you plan to use the vehicle and for how long.

"If you plan to keep a car beyond about five years, owning... tends to be more cost-effective because you eliminate monthly payments and can even recover some of your investment by selling your car later." - ArabWheels

Statistics show that over 60% of car purchases in the UAE are financed through loans, with interest rates ranging from 2.3% to 4.5%. For those considering leasing, used car leases can save up to 40% per month compared to new car leases, depending on factors like the model and mileage.

Platforms like YallaMotor make the process easier with AI-powered valuation tools and transparent listings. Whether you're comparing financing rates from various banks or exploring Sharia-compliant Murabaha options, everything is conveniently accessible in one place. Say goodbye to hidden fees and time-consuming dealership visits.

Start by assessing your car's value, browsing certified listings, and comparing financing or leasing terms that align with your budget. The perfect option is within reach - with the right tools, finding it becomes straightforward.

FAQs

What’s the total cost difference between financing and leasing a used car?

When comparing costs, the difference largely hinges on expenses over time.

Leasing typically comes with lower monthly payments - about 20-30% less than financing. However, it means continuous payments and eventually returning the car unless you decide to buy it at its residual value.

On the other hand, financing demands a higher upfront investment, including a 20% down payment, and may involve steeper interest rates. But once the loan is paid off, the car is yours, which can make it a more cost-effective option in the long run.

How can I improve my chances of used car loan approval in the UAE?

To increase your likelihood of getting approved for a used car loan in the UAE, focus on a few key factors. First, maintain a steady income, a solid credit history, and a manageable debt-to-income ratio. Make sure you have all the necessary documents ready, such as your Emirates ID, passport, UAE driver’s license, recent bank statements, and a salary certificate.

Additionally, providing a down payment of about 20% and selecting a loan tenure that aligns with your financial capacity can make your application more appealing to lenders. These steps can help demonstrate your reliability and ability to repay the loan.

What fees should I budget for besides the down payment?

In addition to the down payment, you’ll need to budget for other expenses like registration, insurance, maintenance, and any potential administrative or processing fees. These costs can differ based on your financing or leasing provider, so it’s worth checking the details upfront.